Sustainability regulation

How to do SFDR Article 8 classification with Upright data

The SFDR delegated regulation entered into force in 2021, providing a definition of sustainable investments under Article 2 (17), and setting the disclosure requirements for funds with sustainability claims. We’ve taken a look at the current market practices around Article 8 classification, and have included our recommendations on how to classify Article 8 funds efficiently and credibly, and what are the main pitfalls to avoid.

Published Apr 24, 2024

Background on SFDR Regulation

+

SFDR in a nutshell

+

Current market practices

+

SFDR fund types

How to define the sustainability approach

Choosing which SFDR fund type to disclose under requires the investor to decide on their sustainability ambition and approach, which should align with the fund’s purpose and investment strategy. Defining the sustainability approach has become more complex as the market has broadened the fund categories. The large variance and the lack of consensus on best practices have also increased the pressure on investors to create robust sustainability approaches.

Essentially, the level of classification is determined by the share of sustainable investments the fund makes. Sustainable investments are defined as “investments that contribute to an environmental or social objective”, without “doing significant harm to any other objective”. Most remaining choices regarding assessing and measuring sustainable investments are left to the investors themselves.

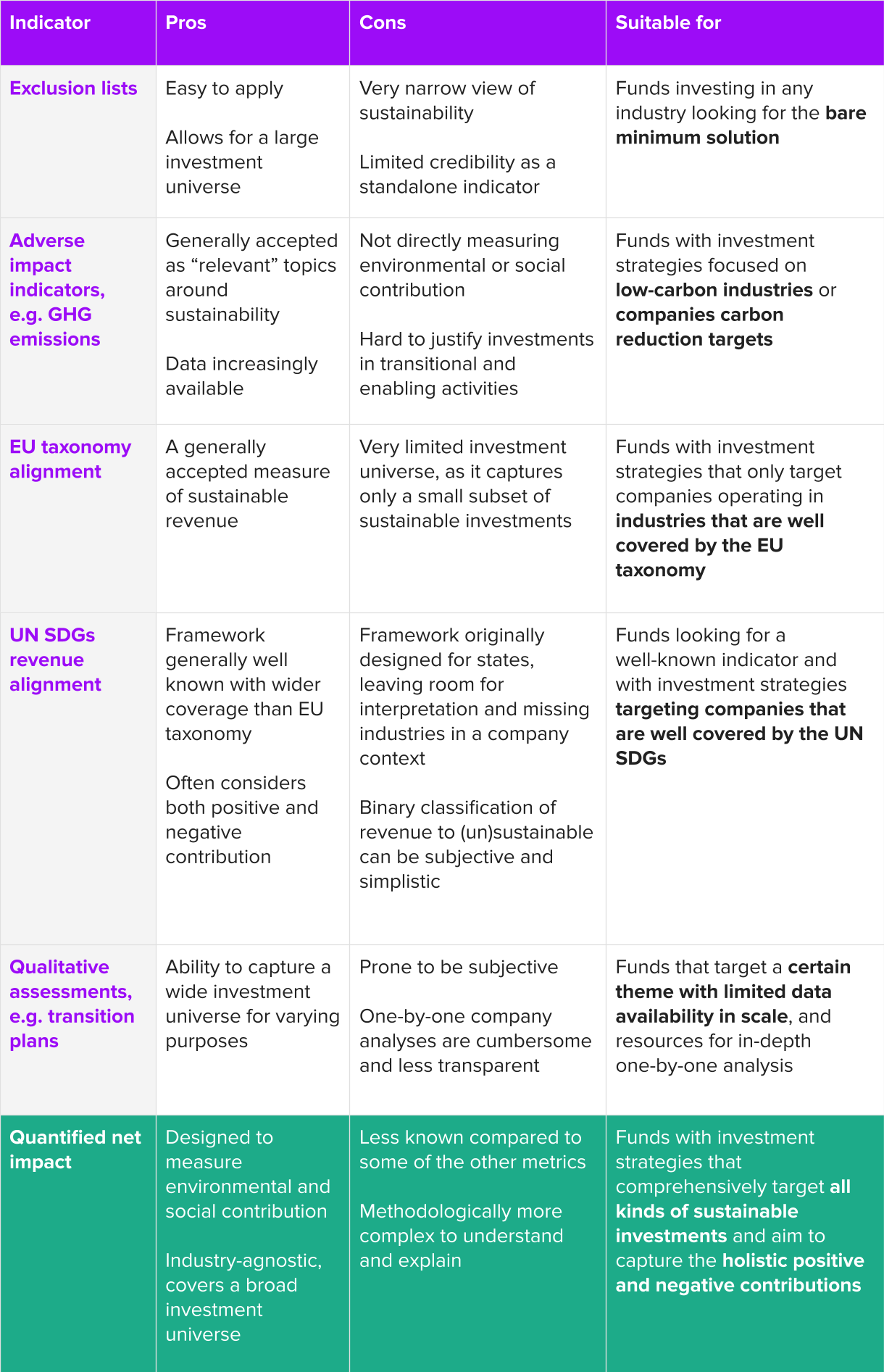

To classify a fund under Article 8 or 9, investors must also choose a sustainability indicator to measure and evaluate its investments' social and environmental characteristics. The decision on the sustainability indicator depends on several criteria such as alignment with investment strategy and fund's mission, credibility among LPs and other stakeholders, and ability to compare between target companies. The table below outlines some of the most typical SI options and their suitability for different purposes.

Learn more about Upright's datasets: Net impact, UN SDG metrics, EU taxonomy metrics, SFDR PAI indicators.

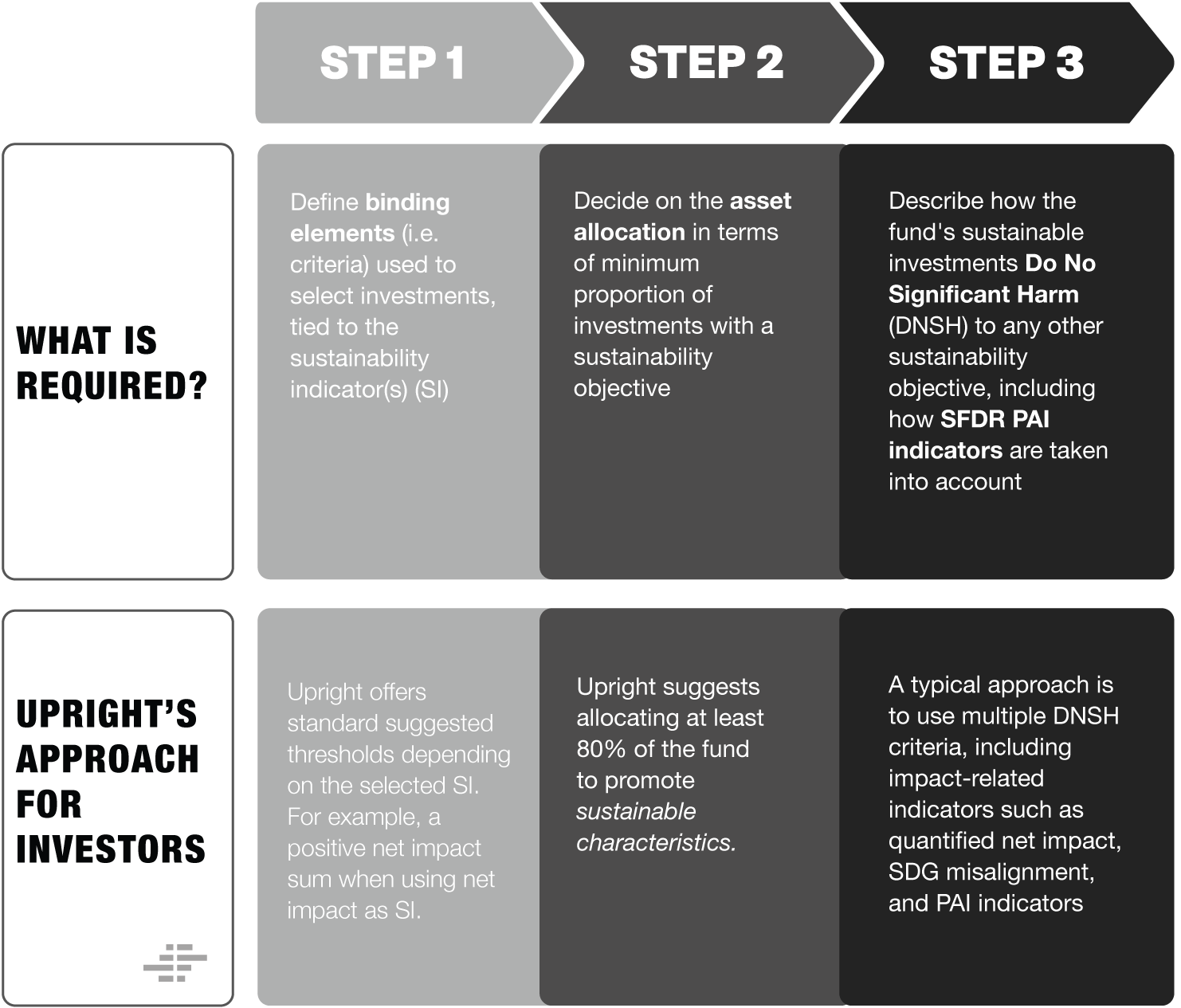

3 concrete steps to classify your fund as Article 8 with Upright's data

Step 1: Define binding elements (thresholds)

After selecting the sustainability indicator, the first concrete classification step is to choose and describe the binding elements (i.e. criteria). This entails deciding, based on the sustainability indicator, what is the threshold for which a company is considered to promote sustainable characteristics. These characteristics can be either environmental or social. However, the SFDR provides limited further clarification on what is meant by sustainability characteristics or how to measure them. The choices related to the criteria of the binding elements are left for the investor to make.

Typical sustainability indicators used in Upright’s approach include quantified net impact and UN SDG revenue alignment. For Article 8 funds, net impact is particularly useful for comprehensively targeting sustainable characteristics across impact categories, and for those with high sustainability ambitions. A typical binding element is an exclusion criterion based on significant negative impacts, which is considered equivalent to the promotion of sustainable characteristics. Using net impact data, this criterion entails that the companies can not have larger negative impacts than set thresholds across each relevant category of the net impact framework.

Investors looking for a more familiar framework may also want to consider the UN SDGs as their SI. The benefit of the SDGs is their understandability, however, they are most suitable for funds targeting industries that are well covered by the goals. Upright provides quantified UN SDG revenue (mis)alignment to all 17 goals. Binding elements for the UN SDGs are usually based on excluding companies with significant misalignments. The thresholds typically range from 20% to 50% revenue misalignment to any UN SDGs.

Step 2: Decide on the asset allocation

Article 8 funds must disclose their asset allocation, in terms of the minimum proportion of investments promoting sustainable characteristics and optionally the proportion of sustainable investments. Typically, Article 8 funds allocate over 80% of their investments towards the promotion of sustainable characteristics. All Article 8 funds are also required to disclose their EU taxonomy-alignment.

Funds that aim for the unofficial and more ambitious Article 8+ category typically allocate a proportion of their funds to sustainable investments. These sustainable investments for Article 8+ follow the same definitions, criteria, and minimum requirements as sustainable investments under Article 9. Upright’s recommendation for Article 8+ funds is to allocate between 10-25% of the fund to sustainable investments.

Step 3: Ensure and show how the fund complies with the DNSH and good governance criteria

Article 8 funds are required to ensure good governance and disclose how Principal Adverse Impacts (PAI) are considered for the investments that promote sustainable characteristics. If the fund additionally makes sustainable investments, that share of the fund must also fulfill the Do No Significant Harm (DNSH) criteria.

It is often best to use multiple layers of data to screen for adverse impacts and ensure good governance. When using net impact data as an example, Upright recommends the use of absolute lower boundaries for certain negative quantified impacts. Further, Article 8 funds should disclose on the Principal Adverse Impact indicators, as part of showing how adverse impacts are considered. These are defined by the Regulatory Technical Standards (RTS) provided by the European Supervisory Authorities (ESA). Upright provides data on all the mandatory and select voluntary PAI indicators, based on a combination of collected and estimated data. A beneficial additional layer of screening is to exclude companies with significant misalignments towards the UN SDGs. Upright provides revenue (mis)alignment towards all the 17 SDGs for this purpose.

What’s next? Please refer to our content around or book a demo

- Indicative guidelines for classifying investments in line with the SFDR in the Upright knowledge base

- Upright’s full impact data offering

- Upright’s full offering for asset managers and private equity

April 24th, 2024

Upright Project

Share: